CONFIDENTIAL COMPLIANCE REVIEW

Collections Ruining Your Credit Score Right Now?

Most people dispute collections the wrong way and stay stuck for months.

The Rx Tri-Sweep™ Blueprint explains the structured escalation approach used to challenge collection reporting step-by-step.

Intro pricing currently $47-Instant download!

Created by Dr. Shereka

Psychiatric Nurse Practitioner & Credit Strategy Educator

This educational blueprint explains structured compliance escalation methods used in real dispute cases.

Why Most Disputes Fail

Template disputes trigger automated responses.

Creditors often verify without deep investigation.

Consumers repeat the same steps expecting new outcomes.

If this sounds familiar, it's not because credit repair "doesn't work." It's because most people are never taught the structured escalation process that triggers real investigation.

Real Credit Report Results

These are real structured escalation outcomes-not theory.

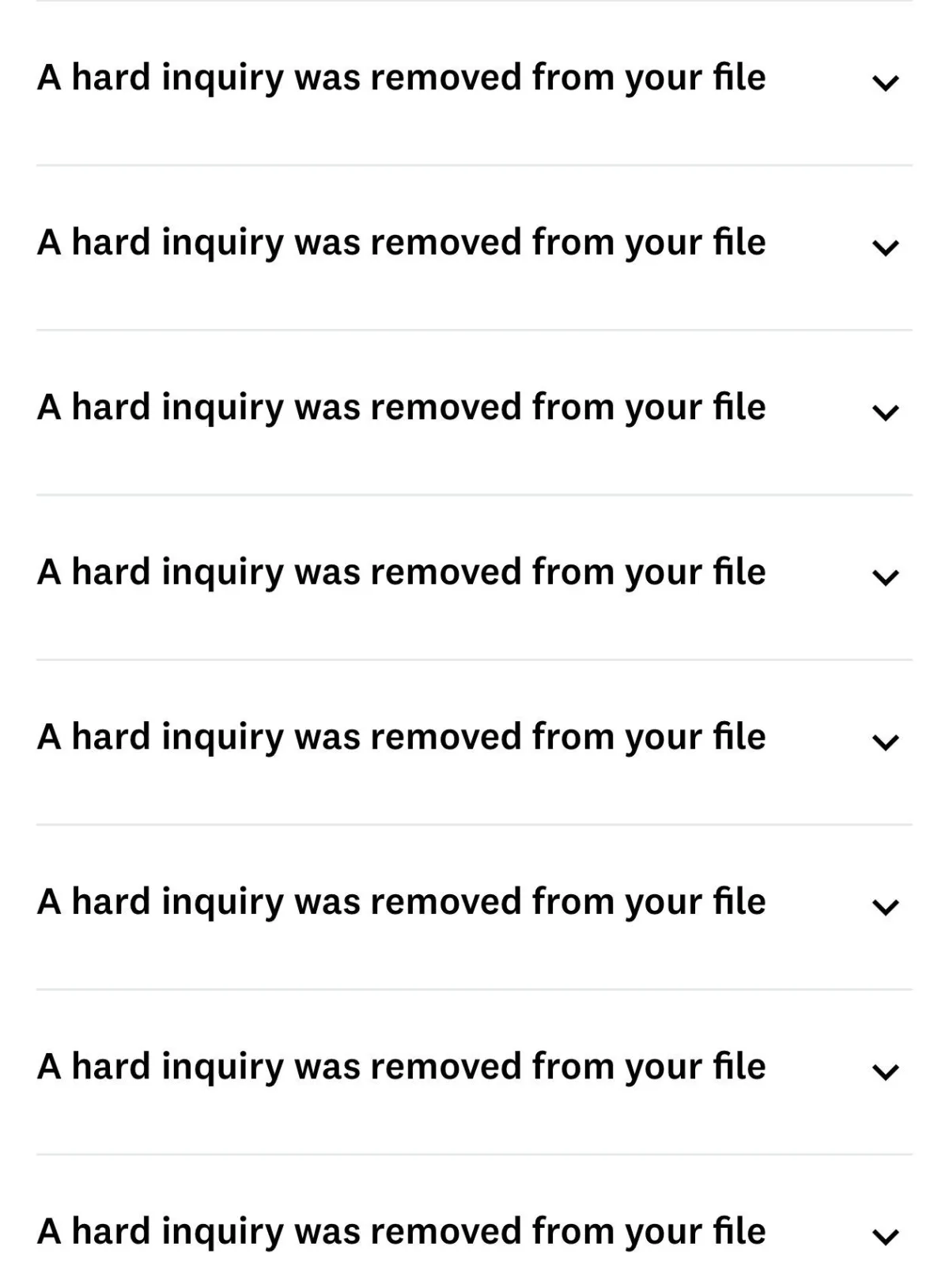

20+ Hard Inquiries Removed

Example of multiple hard inquiries removed after structured compliance escalation.

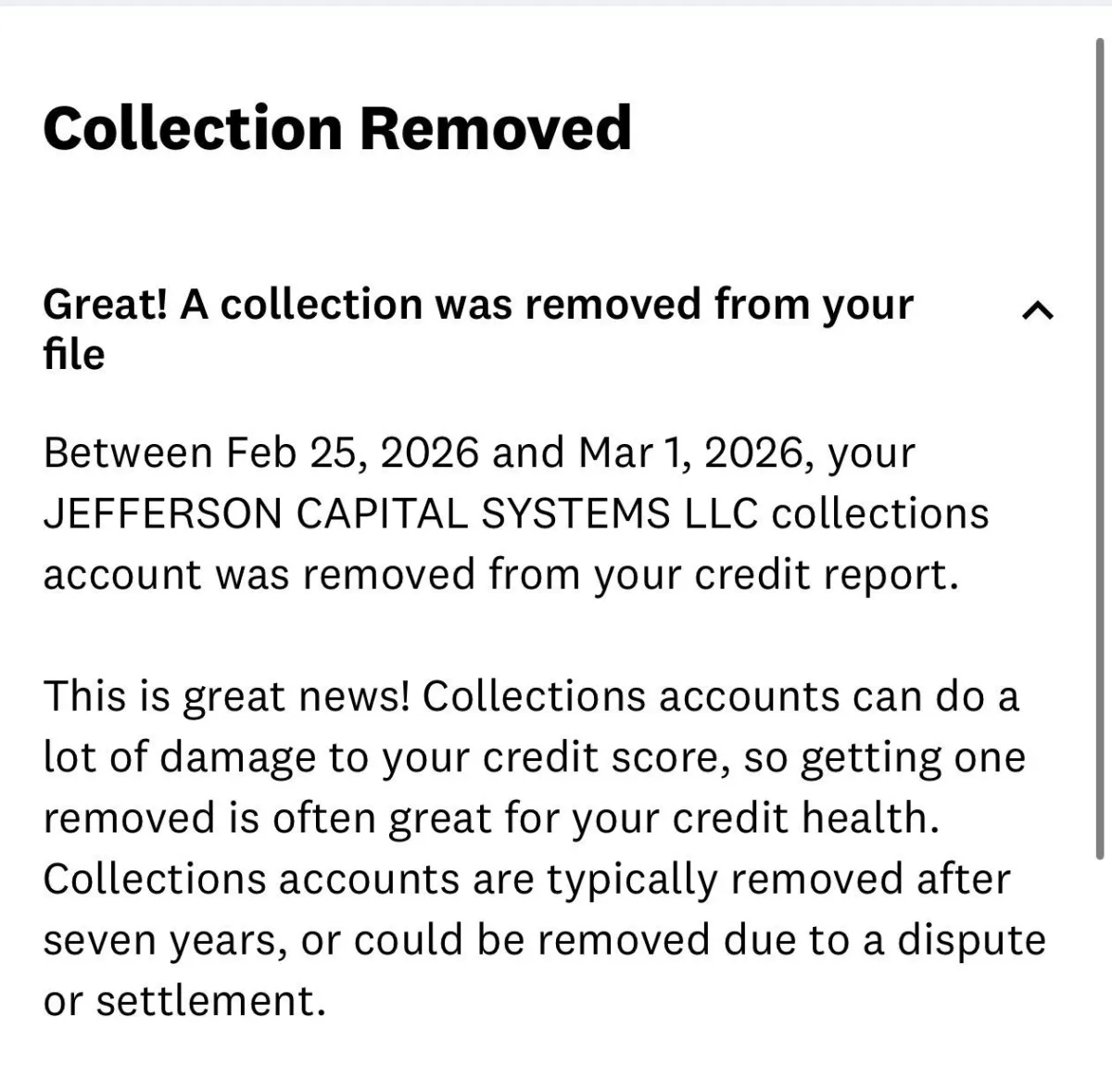

Collection Account Removed

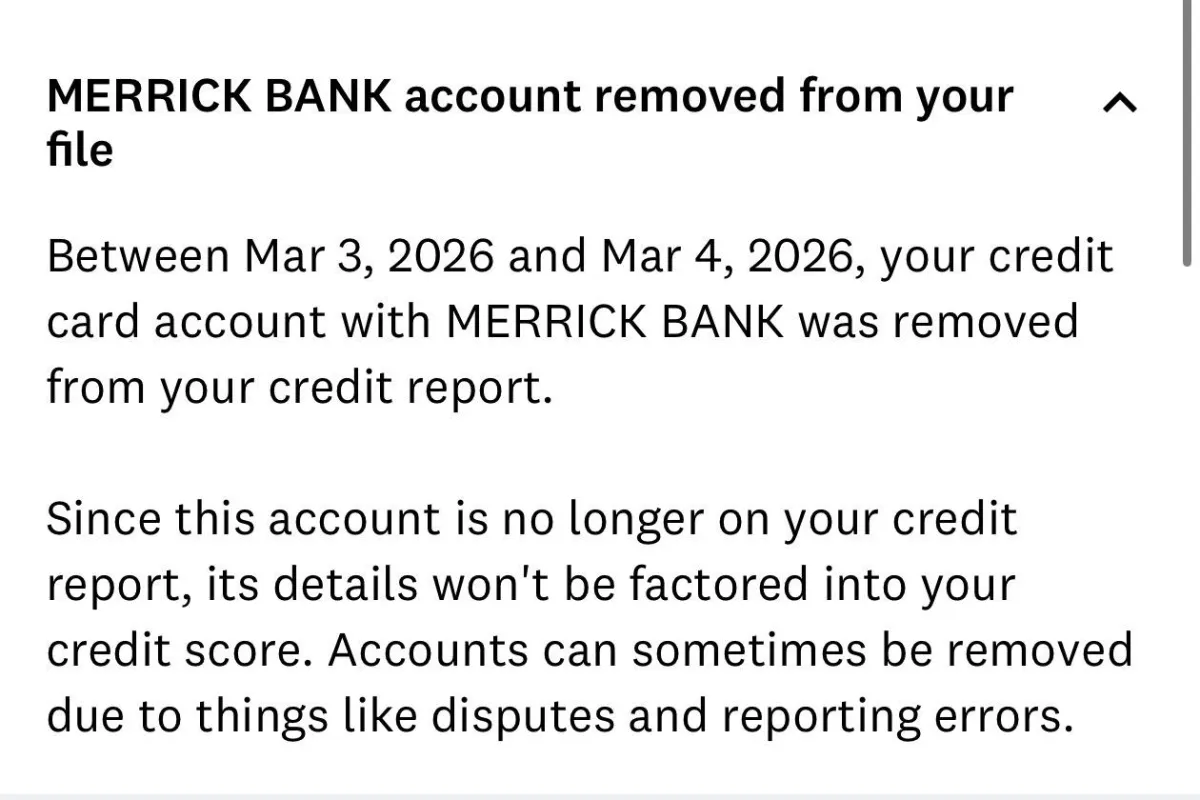

Merrick Bank Account Removed

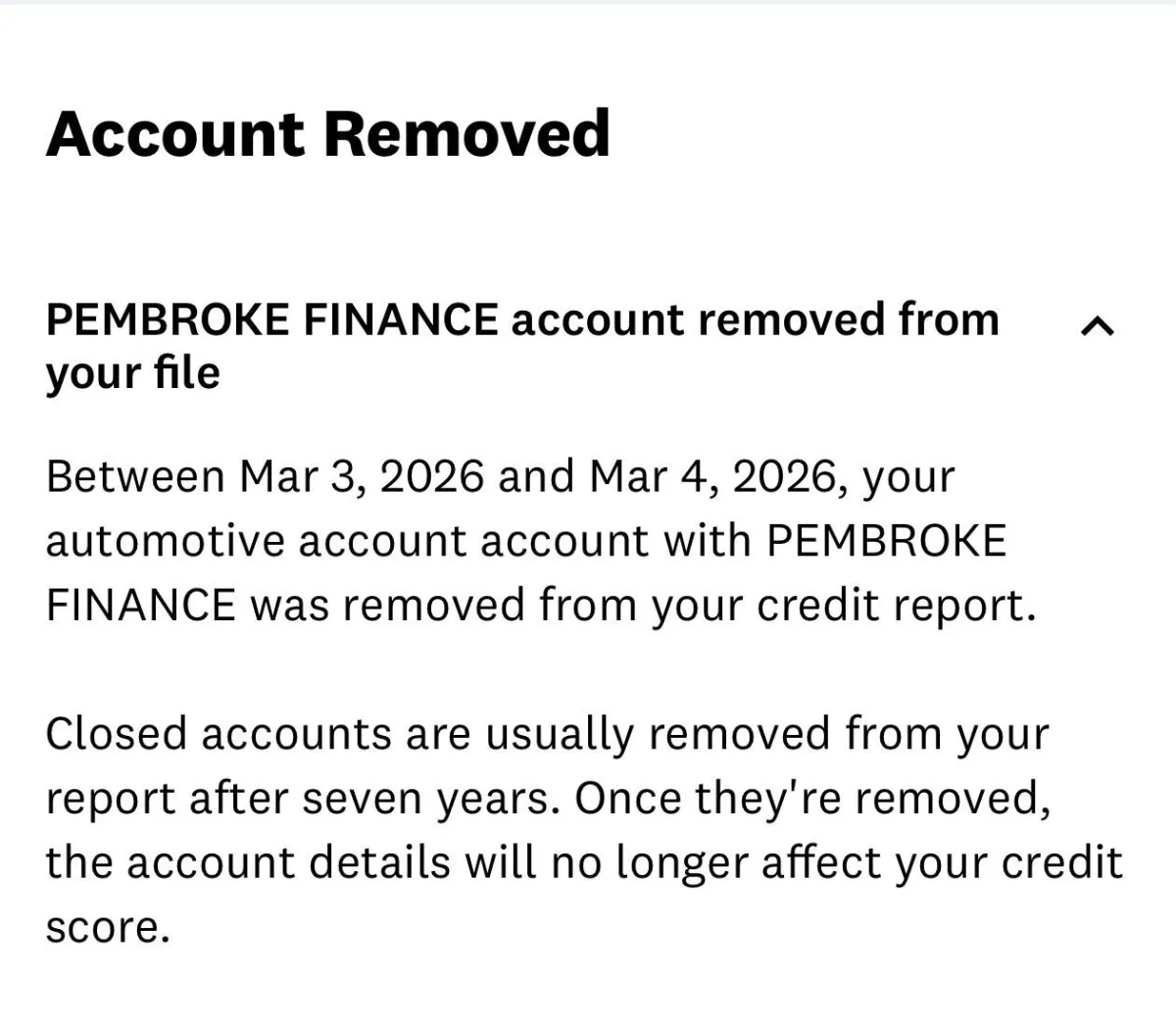

Pembroke Finance Account Removed

They Rely on Automation

Most agencies push disputes through software — not real human review.

You Can Trigger

Real Review

When escalated properly, agencies must conduct a real compliance investigation.

Compliance Forces Accountability

When compliance standards are invoked, agencies must document their investigation and validate the account properly.

Force Real Compliance

Within 72 Hours

Stop waiting 30-45 days for automated responses.

Trigger documented human review immediately.

If you have a collection account reporting on your credit file, this breakdown shows you how structured escalation works.

Download the Rx Tri-Sweep™ Blueprint Now

Unlock the 3-Step Collection Strategy

Submit your information below to begin a structured compliance review of your credit report.

✔ No Template Mailing Letters

✔ No 45-Day Waiting Games

✔ Structured for Real Compliance Leverage

This is Not a Template Letter Program

Template letters get filtered.

Structured compliance escalation gets reviewed.

Every submission is built to force documented human evaluation under federal standards.

How the 72-Hour Review Works

Every situation is different, which is why each submission is reviewed individually before any action is taken.

The 72-Hour Review evaluates the reporting structure, compliance posture, and escalation options available under federal consumer protection standards.

If a viable escalation path exists, the next steps will be clearly outlined.

✓ Submit your information for review

✓ We evaluate the reporting structure and compliance posture

✓ You receive your escalation options within 72 hours

✓ No automated template disputes

✓ No mailing letters

✓ No 45-day waiting periods

Who This Review is For

This review is designed for individuals dealing with inaccurate credit reporting or disputes that have already been ignored or rejected.

If your situation requires structured escalation under federal consumer protection standards, the next steps will be clearly outlined after the review.

✓ Individuals dealing with inaccurate credit reporting

✓ Situations where previous disputes were ignored or rejected

✓ Consumers seeking structured compliance escalation options

What Happens After You Submit

Once your information is submitted, it is reviewed to determine whether a viable compliance escalation path exists.

If escalation options are available, you will receive a clear outline of the next steps and the documentation required to proceed.

✓ Your submission is reviewed individually

✓ Reporting and compliance structure is evaluated

✓ Escalation options are delivered within 72 hours

Start Your 72-Hour Review

Submit your information to begin the review process.

If a structured escalation path exists, the next steps will be outlined clearly.